主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2024, Vol. 32 ›› Issue (1): 54-64.doi: 10.16381/j.cnki.issn1003-207x.2021.1041cstr: 32146.14.j.cnki.issn1003-207x.2021.1041

白兰,魏宇( )

)

收稿日期:2021-05-27

修回日期:2022-06-24

出版日期:2024-01-25

发布日期:2024-02-08

通讯作者:

魏宇

E-mail:weiyusy@126.com

基金资助:

Lan Bai,Yu Wei()

Received:2021-05-27

Revised:2022-06-24

Online:2024-01-25

Published:2024-02-08

Contact:

Yu Wei

E-mail:weiyusy@126.com

摘要:

2019年年末的突发公共卫生事件对我国金融市场产生了前所未有的巨大冲击,期间投资者对该事件流行态势的关注度(情绪)对我国股票市场的影响作用不容小觑。因此,探讨在此次突发公共卫生事件的不同阶段投资者关注度与我国不同行业股票市场间的相互作用,对政策制定者和各类市场主体来说无疑都具有极其重要的理论和现实意义。在传统静态溢出指数(Spillover Index)基础上,本文运用基于时变参数-向量自回归模型(TVP-VAR)的动态溢出指数法,探究了我国从公共卫生事件前到事件爆发并快速蔓延,再到防控常态化的三个不同阶段下投资者关注与我国不同行业股票市场间的信息动态溢出方向及其强度。实证结果表明,一方面,基于百度搜索指数的投资者关注度在公共卫生事件不同阶段与行业股票市场间的信息溢出作用具有显著差异;另一方面,工业和可选消费行业股票在各阶段始终是信息的发出者,而医药和公用行业股票则基本保持信息接收的状态。上述发现可以为监管者、上市公司和投资者的风险防控措施及投资组合管理等问题提供科学的决策依据。

中图分类号:

白兰,魏宇. 投资者公共卫生事件关注度与我国行业股票市场信息溢出效应研究[J]. 中国管理科学, 2024, 32(1): 54-64.

Lan Bai,Yu Wei. Information Spillovers between Investor's Public Health Emergency Attention and Industrial Stocks: Empirical Evidence from TVP-VAR Model[J]. Chinese Journal of Management Science, 2024, 32(1): 54-64.

表1

相关数据的描述性统计"

| 统计量 | 能源 | 工业 | 可选 | 医药 | 信息 | 公用 | 百度 |

|---|---|---|---|---|---|---|---|

| 均值 | 0.0025 | 0.1107 | 0.1567 | 0.1694 | 0.1497 | 0.0059 | -3.1291 |

| 标准差 | 1.2536 | 1.4399 | 1.6519 | 1.6900 | 2.0910 | 0.9421 | 11.8240 |

| 偏度 | -0.3445*** | -0.5481*** | -0.7347*** | -0.3814*** | -0.4944*** | -0.0780 | 3.0957*** |

| 峰度 | 5.5432*** | 4.9129*** | 3.0499*** | 0.8574*** | 2.1131*** | 1.5554*** | 27.0706*** |

| J-B | 672.1314*** | 545.8291*** | 246.8888*** | 28.3716*** | 117.2563*** | 52.6381*** | 16611.8711*** |

| Q(5) | 6.5790 | 6.5890 | 4.3820 | 1.9060 | 4.8440 | 6.1490 | 11.4250** |

| Q(20) | 23.0740 | 23.5450 | 16.3060 | 29.6200 | 17.4540 | 16.5020 | 77.1500*** |

| ADF | -21.1394*** | -21.7964*** | -22.3128*** | -22.3715*** | -22.1220*** | -22.8172*** | -20.3169*** |

| P-P | -21.1788*** | -21.8392*** | -22.3567*** | -22.4165*** | -22.1657*** | -22.8616*** | -20.3539*** |

表2

第一阶段信息溢出强度(疫情爆发前的平稳阶段)"

| 行业 | 能源 | 工业 | 可选 | 医药 | 信息 | 公用 | 百度 | FROM |

|---|---|---|---|---|---|---|---|---|

| 能源 | 32.6 | 20.6 | 13.1 | 8.6 | 12.2 | 11.4 | 1.3 | 9.6 |

| 工业 | 16.7 | 26.1 | 16.7 | 11.7 | 16.8 | 11.2 | 0.8 | 10.6 |

| 可选 | 12.4 | 19.1 | 30.2 | 15.2 | 13.2 | 9.2 | 0.7 | 10.0 |

| 医药 | 9.5 | 15.4 | 17.7 | 35.3 | 13.7 | 7.6 | 0.9 | 9.2 |

| 信息 | 11.8 | 20.0 | 13.8 | 12.3 | 31.8 | 9.4 | 0.8 | 9.7 |

| 公用 | 13.4 | 16.2 | 11.2 | 8.2 | 12.0 | 37.6 | 1.4 | 8.9 |

| 百度 | 2.8 | 2.4 | 1.8 | 2.1 | 2.0 | 2.8 | 86.1 | 2.0 |

| TO | 9.5 | 13.4 | 10.6 | 8.3 | 10.0 | 7.4 | 0.9 | 60.0 |

| NET | -0.1 | 2.8 | 0.6 | -0.9 | 0.2 | -1.5 | -1.1 |

表3

第二阶段信息溢出强度(疫情爆发后的快速扩散阶段)"

| 行业 | 能源 | 工业 | 可选 | 医药 | 信息 | 公用 | 百度 | FROM |

|---|---|---|---|---|---|---|---|---|

| 能源 | 20.9 | 18.0 | 16.5 | 10.8 | 10.7 | 16.8 | 6.3 | 11.3 |

| 工业 | 17.3 | 20.1 | 17.0 | 11.6 | 12.3 | 15.9 | 5.8 | 11.4 |

| 可选 | 15.6 | 16.6 | 19.7 | 14.2 | 15.0 | 13.7 | 5.2 | 11.5 |

| 医药 | 12.5 | 13.8 | 17.6 | 25 | 13.9 | 12.8 | 4.5 | 10.7 |

| 信息 | 12.7 | 15.0 | 18.5 | 13.9 | 24.3 | 11.4 | 4.3 | 10.8 |

| 公用 | 17.3 | 17.0 | 15.3 | 11.9 | 10.7 | 21.9 | 5.9 | 11.2 |

| 百度 | 4.4 | 4.2 | 4.5 | 6.3 | 1.7 | 7.0 | 71.9 | 4.0 |

| TO | 11.4 | 12.1 | 12.8 | 9.8 | 9.2 | 11.1 | 4.6 | 70.9 |

| NET | 0.1 | 0.7 | 1.3 | -0.9 | -1.6 | -0.1 | 0.5 |

表4

第三阶段信息溢出强度(疫情防控常态化阶段)"

| 行业 | 能源 | 工业 | 可选 | 医药 | 信息 | 公用 | 百度 | FROM |

|---|---|---|---|---|---|---|---|---|

| 能源 | 46.2 | 17.2 | 11.2 | 2.0 | 8.0 | 12.9 | 2.6 | 7.7 |

| 工业 | 12.2 | 33.5 | 19.6 | 10.4 | 17.1 | 6.4 | 0.7 | 9.5 |

| 可选 | 8.4 | 21.3 | 36.8 | 10.4 | 17.1 | 4.4 | 1.7 | 9.0 |

| 医药 | 2.0 | 14.3 | 12.7 | 53.0 | 14.7 | 2.7 | 0.7 | 6.7 |

| 信息 | 7.0 | 19.8 | 17.5 | 11.4 | 38.4 | 4.8 | 1.1 | 8.8 |

| 公用 | 15.8 | 10.3 | 6.1 | 3.4 | 6.8 | 54.7 | 3.0 | 6.5 |

| 百度 | 4.3 | 2.7 | 3.9 | 1.6 | 2.6 | 5.3 | 79.7 | 2.9 |

| TO | 7.1 | 12.2 | 10.2 | 5.6 | 9.5 | 5.2 | 1.4 | 51.1 |

| NET | -0.6 | 2.7 | 1.1 | -1.1 | 0.7 | -1.3 | -1.5 |

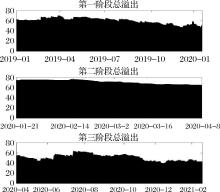

图1

三阶段信息总溢出强度的动态变化情况注:图中三个阶段分别为疫情爆发前的平稳阶段、疫情爆发后的快速扩散阶段和疫情防控常态化阶段。"

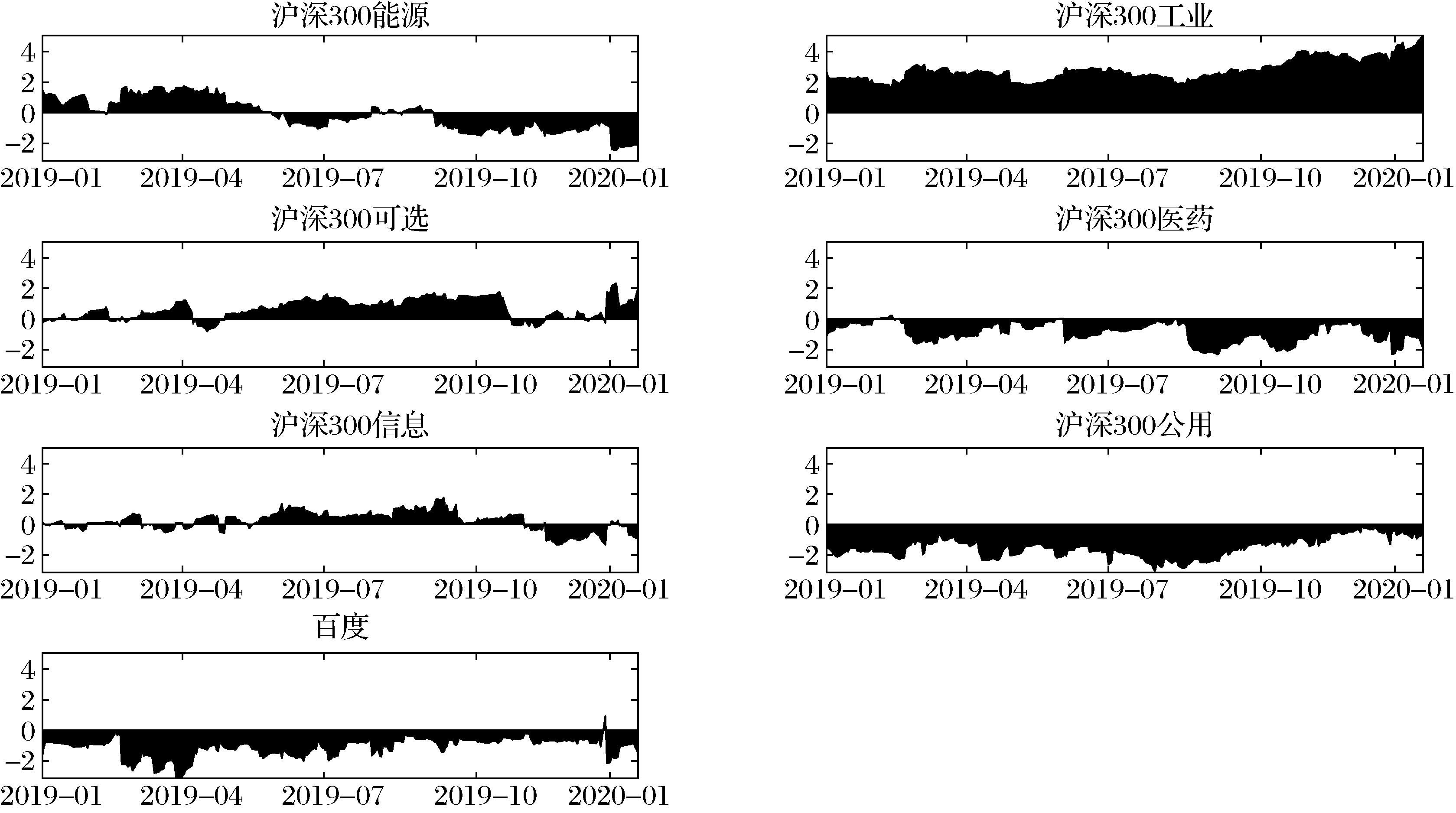

图2

第一阶段(疫情爆发前的平稳阶段)净溢出动态变化"

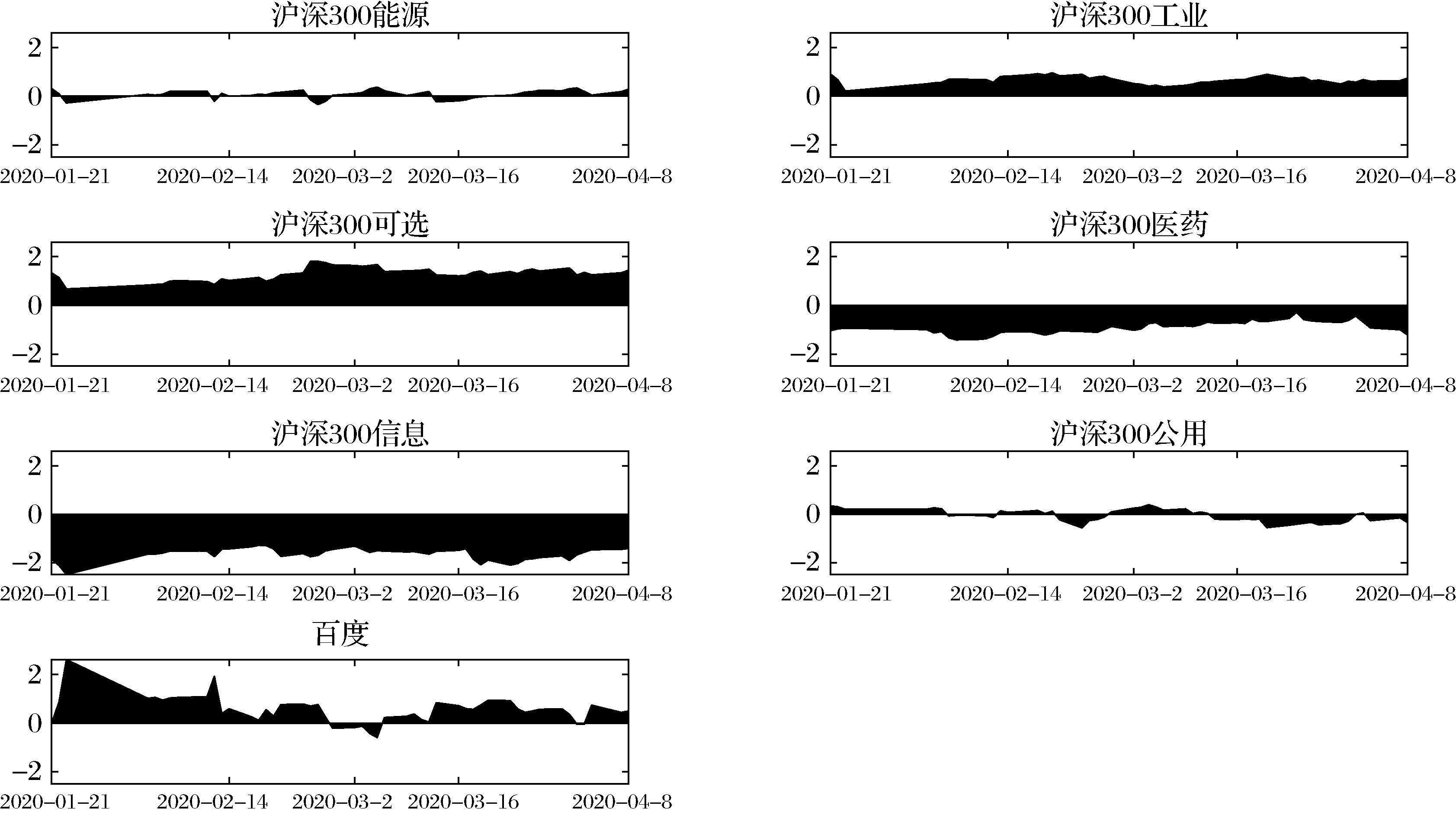

图3

第二阶段(疫情爆发后的快速扩散阶段)净溢出动态变化"

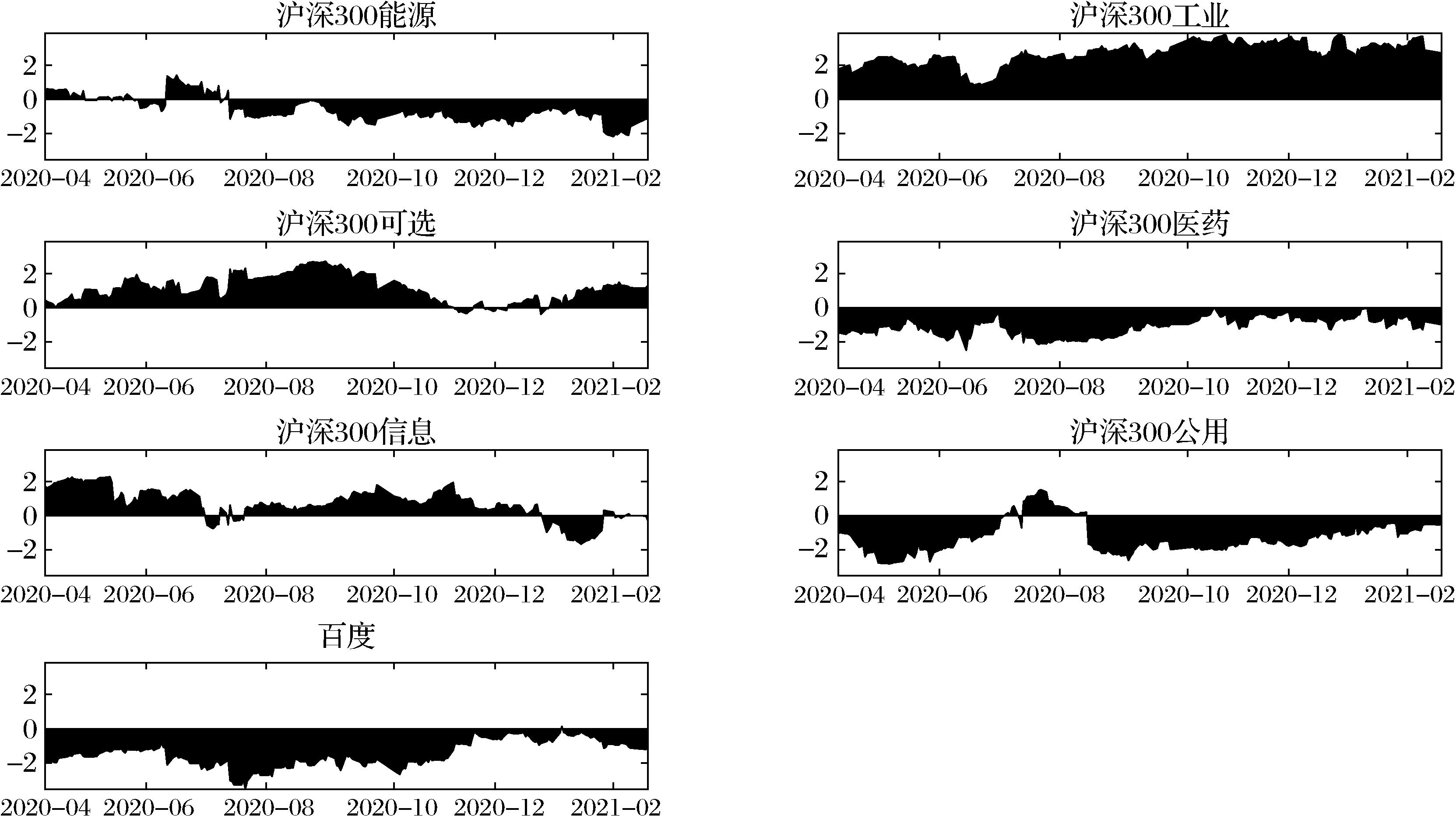

图4

第三阶段(疫情防控常态化阶段)净溢出动态变化"

| 1 | 方意, 于渤, 王炜.新冠疫情影响下的中国金融市场风险度量与防控研究[J].中央财经大学学报,2020(8): 116-128. |

| Fang Y, Yu B, Wang W. China’ s financial market risk measurement and controlling under covid-19 shock[J]. Journal of Central University of Finance and Economics,2020(8): 116-128. | |

| 2 | 杨子晖, 陈雨恬, 张平淼.重大突发公共事件下的宏观经济冲击、金融风险传导与治理应对[J].管理世界,2020, 36(5): 13-35+7. |

| Yang Z H, Chen Y T, Zhang P M. Macroeconomic shock, financial risk transmission and governance response to major public emergencies[J]. Journal of Management World,2020, 36(5): 13-35+7. | |

| 3 | 蒋海, 吴文洋, 韦施威.新冠肺炎疫情对全球股市风险的影响研究——基于ESA方法的跨市场检验[J].国际金融研究,2021(3): 3-13. |

| Jiang H, Wu W Y, Wei S W. Research on the impact of COVID-19 on the risks of global stock market: cross market test based on ESA method[J]. Studies of International Finance,2021(3): 3-13. | |

| 4 | Bouri E, Cepni O, Gabauer D, et al.Return connectedness across asset classes around the COVID-19 outbreak[J].International Review of Financial Analysis,2021, 73,101646. |

| 5 | 张宗新, 王海亮.投资者情绪、主观信念调整与市场波动[J].金融研究,2013(4): 142-155. |

| Zhang Z X, Wang H L. Investor sentiment, subjective belief adjustment and market fluctuation[J]. Journal of Financial Research,2013(4): 142-155. | |

| 6 | 唐振鹏, 吴俊传, 冉梦, 等.考虑投资者情绪的中国股市自激发效应研究[J].中国管理科学,2020, 28(7): 1-12. |

| Tang Z P, Wu J C, Ran M, et al. Research on the self-exciting effect of Chinese stock market considering investor sentiment[J]. Chinese Journal of Management Science,2020, 28(7): 1-12. | |

| 7 | 张国胜, 林宇.结构突变下投资者情绪与股市收益间的非线性溢出效应研究[J].数理统计与管理,2021, 40 (1): 148-161. |

| Zhang G S, Lin Y. Research on non-liner information spillover effect between investor sentiment and stock market return under structural break[J]. Journal of Applied Statistics and Management,2021, 40(1): 148-161. | |

| 8 | Al-Awadhi A M, Alsaifi K, Al-Awadhi A, et al.Death and contagious infectious diseases: impact of the COVID-19 virus on stock market returns[J].Journal of Behavioral and Experimental Finance,2020, 27: 100326. |

| 9 | Pham A V, Adrian C, Garg M, et al.State-level COVID-19 outbreak and stock returns[J].Finance Research Letters,2021, 43: 102002. |

| 10 | 易行健.新冠肺炎疫情对经济金融的冲击研究——基于国际文献综述及其扩展分析[J].金融经济学研究,2020, 35(3): 3-16. |

| Yi X J. The economic and financial impacts of the COVID-19 pandemic: discussions based on international literature review and related conclusions[J]. Financial Economics Research,2020, 35(3): 3-16. | |

| 11 | 程晨, 刘珂.新冠肺炎疫情下资本市场的冲击研究——基于股价同步性视角[J].工业技术经济,2021, 40(3): 125-135. |

| Cheng C, Liu K. Research on the impact of capital markets under COVID-19: based on stock price synchronization[J]. Journal of Industrial Technological Economics,2021, 40(3): 125-135. | |

| 12 | 陈奉功.新冠肺炎疫情对我国企业的异质性影响——基于股价波动视角的实证研究[J].工业技术经济,2020, 39(10): 3-14. |

| Chen F G.The heterogeneous impact of COVID-19 on chinese enterprises: empirical research based on the perspective of stock price fluctuations[J]. Journal of Industrial Technological Economics,2020, 39(10): 3-14. | |

| 13 | 田金方, 杨晓彤, 薛瑞, 等. 不确定性事件、投资者关注与股市异质特征——以COVID-19概念股为例[J].财经研究,2020, 46 (11): 19-33. |

| Tian J F, Yang X T, Xue R, et al. Uncertain event,investor attention and heterogeneity of the stock market:a case study on COVID-19[J]. Journal of Finance and Economics,2020, 46 (11): 19-33. | |

| 14 | 巫细波, 张小英, 葛志专, 等.我国COVID-19疫情时空演变特征研究——基于314个城市329天面板数据[J].地域研究与开发,2021, 40(1): 1-6. |

| Wu X B, Zhang X Y, Ge Z Z, et al. Study on characteristics of spatio-temporal evolution of COVID-19 epidemic in china: based on 329 days panel data of 314 cities[J]. Areal Research and Development,2021, 40(1): 1-6. | |

| 15 | 张建平, 朱雅锡.后疫情时代下新冠肺炎疫情对中国服务经济影响——基于多期双重差分模型的研究[J].工业技术经济,2021, 40(4): 58-67. |

| Zhang J P, Zhu Y X. The impact of COVID-19 epidemic on china's service economy in post epidemic era: a study based on a multi period double difference model[J].Journal of Industrial Technological Economics,2021, 40(4): 58-67. | |

| 16 | 王箐, 王钟黎, 李士雪, 等.“新冠肺炎”疫情对中国股市价格波动的短期影响[J].经济与管理评论,2020, 36(6): 16-27. |

| Wang Q, Wang Z L, Li S X, et al. The immediate impact of COVID-19 on china’s stock price fluctuation[J]. Review of Economy and Management,2020, 36(6): 16-27. | |

| 17 | Baig A S, Butt H A, Haroon O, et al.Deaths, panic, lockdowns and US equity markets: The case of COVID-19 pandemic[J].Finance Research Letters,2021,38: 101701. |

| 18 | 陈林, 曲晓辉.传染性公共卫生事件的市场反应研究——基于新冠肺炎疫情对中国股市的影响[J].金融论坛,2020, 25(7): 25-33+65. |

| Chen L, Qu X H. Market response to contagious public health events:a research based on COVID-19’s impact on chinese stock market[J]. Finance Forum,2020, 25(7): 25-33+65. | |

| 19 | Primiceri G E.Time varying structural vector autoregressions and monetary policy[J].Review of Economic Studies,2005, 72(3): 821-852. |

| 20 | Wen F H, Zhang M Z, Deng M, et al.Exploring the dynamic effects of financial factors on oil prices based on a TVP-VAR model[J].Physica A-Statistical Mechanics and Its Applications,2019, 532: 121881. |

| 21 | 袁晨, 傅强, 彭选华.我国股票与债券、黄金间的资产组合功能研究——基于DCC-MVGARCH模型的动态相关性分析[J].数理统计与管理,2014, 33(4): 714-723. |

| Yuan C, Fu Q, Peng X H. Research on the portfolio implications of stocks, bonds and gold in china——an analysis of dynamic relationships based on DCC-MVGARCH model[J]. Journal of Applied Statistics and Management,2014, 33(4): 714-723. | |

| 22 | 曹栋, 张佳.基于GARCH-M模型的股指期货对股市波动影响的研究[J].中国管理科学,2017, 25(1): 27-34. |

| Cao D, Zhang J. The impact of index future on stock market volatility based on the GARCH-M-model[J].Chinese Journal of Management Science,2017, 25(1): 27-34. | |

| 23 | 周开国, 邢子煜, 彭诗渊.中国股市行业风险与宏观经济之间的风险传导机制[J].金融研究,2020(12): 151-168. |

| Zhou K G, Xing Z Y, Peng S Y. The contagion mechanism between industrial risk and the macro economy in china[J]. Journal of Financial Research,2020(12): 151-168. | |

| 24 | 蔚立柱, 赵越强, 张凡, 等.新冠肺炎疫情前后人民币与非美货币溢出效应特征的变化:来自30分钟高频数据的证据[J].世界经济研究,2021(4): 56-69+135. |

| Wei L Z, Zhao Y Q, Zhang F, et al. The change of the spillover effect of rmb and non us currency before and after the COVID-19: evidence from 30 minutes high frequency data[J]. World Economy Studies,2021(4): 56-69+135. | |

| 25 | Diebold F X, Yilmaz K.On the network topology of variance decompositions: measuring the connectedness of financial firms[J].Journal of Econometrics,2014, 182 (1): 119-134. |

| 26 | Antonakakis N, Chatziantoniou I, Gabauer D.Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions[J].Journal of Risk and Financial Management,2020, 13(4): 84. |

| 27 | Esmaeili P, Rafei M.Dynamics analysis of factors affecting electricity consumption fluctuations based on economic conditions: application of SVAR and TVP-VAR models[J].Energy,2021, 226: 120340. |

| 28 | 刘金全, 王国志.金融周期与经济周期关联机制研究——基于DY动态溢出指数和时变格兰杰因果关系双重检验[J].暨南学报(哲学社会科学版),2021, 43(4): 84-99. |

| Liu J Q, Wang G Z. Research on the correlation mechanism between financial cycle and business cycle: double test based on dy dynamic spillover index and time-varying granger causality[J]. Jinan Journal(Philosophy & Social Sciences),2021, 43(4): 84-99. | |

| 29 | Nakajima J, Kasuya M, Watanabe T.Bayesian analysis of time-varying parameter vector autoregressive model for the Japanese economy and monetary policy[J].Journal of the Japanese and International Economies,2011, 25(3): 225-245. |

| 30 | Belomestny D, Krymova E, Polbin A.Bayesian TVP-VARX models with time invariant long-run multipliers[J].Economic Modelling,2021, 101: 105531. |

| 31 | 赵儒煜, 聂逯松.“双循环”背景下国际贸易冲击的宏观经济效应——理论模拟与动态计量检验[J].经济问题探索,2021(5): 136-145. |

| Zhao R Y, Nie L S. Macroeconomic effects of international trade shocks under the background of “double cycle” ——theoretical simulation and dynamic empirical analysis[J]. Inquiry into Economic Issues,2021(5): 136-145. | |

| 32 | 任永平, 李伟.经济政策不确定性、投资者情绪与股价同步性——基于TVP-VAR模型的时变参数[J].上海大学学报(自然科学版),2020, 26(5): 769-781. |

| Ren Y P, Li W. Economic policy uncertainty, investor’s sentiment and stock price synchronicity: a time-varying analysis based on TVP-VAR model[J]. Journal of Shanghai University(Natural Science Edition),2020, 26(5): 769-781. | |

| 33 | 姜伟.突发大规模疫情对经济发展的影响——基于公众关注和媒体关注的视角[J].经济与管理研究,2020, 41(10): 21-41. |

| Jiang W. The Impact of the large-scale epidemic outbreak on economic growth—based on the public and media attention[J]. Research on Economics and Management,2020, 41(10): 21-41. | |

| 34 | 张同辉, 苑莹, 曾文.投资者关注能提高市场波动率预测精度吗?——基于中国股票市场高频数据的实证研究[J].中国管理科学,2020, 28(11): 192-205. |

| Zhang T H, Yuan Y, Zeng W. Can investor attention help to predict stock market volatility? An empirical research based on chinese stock market high-frequency data[J]. Chinese Journal of Management Science,2020, 28(11): 192-205. | |

| 35 | 林娟娟, 唐勇, 周小亮,等.北上资金、百度指数与股市关联性的时频域研究——基于协高阶矩视角[J].中国管理科学,2022, 30(1): 20-31. |

| Lin J J, Tang Y, Zhou X L, et al. Research on the relationship between northward capital, baidu index and stock market in time and frequency domain——based on the perspective of higher order co-moments[J].Chinese Journal of Management Science,2022, 30(1): 20-31. | |

| 36 | 刘晓君, 姜伟, 胡劲松.基于TVP-VAR模型的信心、货币政策与中国经济波动研究[J].中国管理科学,2019, 27(8): 37-46. |

| Liu X J, Jiang W, Hu J S. A study on confidence, monetary policy and China’s economic fluctuation based on TVP-VAR model[J].Chinese Journal of Management Science,2019, 27(8): 37-46. | |

| 37 | 齐红倩, 刘岩.人口年龄结构变动对经常账户和经济增长的动态影响研究——基于TVP-VAR模型的实证分析[J].中南大学学报(社会科学版),2020,26 (6): 90-102. |

| Qi H Q, Liu Y. Research on the dynamic effects of changes in population age structure on current account and economic growth: empirical analysis based on TVP-VAR model[J]. Journal of Central South University (Social Sciences),2020, 26(6): 90-102. | |

| 38 | 李成刚, 李峰, 赵光辉.货币政策规则对国际资本流动与人民币汇率的时变影响——基于TVP-SV-VAR模型的实证检验[J].中国管理科学,2021, 29(10): 35-46. |

| Li C G, Li F, Zhao G H. The time-varying effects of monetary policy rules on international capital flow and rmb exchange rate: empirical test based on TVP-SV-VAR model[J]. Chinese Journal of Management Science,2021, 29(10): 35-46. | |

| 39 | 杨涛, 郭萌萌.投资者关注度与股票市场——以PM2.5概念股为例[J].金融研究,2019(5): 190-206. |

| Yang T, Guo M M. Investor attention and the stock market: a new perspective on pm2.5 concept stocks[J]. Journal of Financial Research,2019(5): 190-206. | |

| 40 | 梁超, 魏宇, 马锋, 等.投资者关注对中国黄金价格波动率的影响研究[J].系统工程理论与实践,2022, 42(2): 320-332. |

| Liang C, Wei Y, Ma F, et al. A study on the impact of investor attention on Chinese gold volatility[J]. Systems Engineering—Theory & Practice, 2022, 42(2): 320-332 . |

| [1] | 石松,石平. 疫情背景下考虑社会学习的竞争防疫产品供应中断研究[J]. 中国管理科学, 2024, 32(5): 171-178. |

| [2] | 陈凤娇,刘德海. 重大传染病多渠道疫情信息发布模式的演化路径分析[J]. 中国管理科学, 2024, 32(4): 237-249. |

| [3] | 贾芳菊,周坤,李廉水. 突发公共卫生事件协同防控策略的随机演化决策分析[J]. 中国管理科学, 2024, 32(3): 237-247. |

| [4] | 张桂蓉,董志香,夏霆. 突发公共卫生事件网络谣言网格化预警模型研究[J]. 中国管理科学, 2024, 32(2): 298-306. |

| [5] | 朱宏淼, 闫辛, 齐佳音, 靳祯. 社会民众新冠病毒疫苗接种意识传播模型与干预策略研究[J]. 中国管理科学, 2023, 31(8): 269-277. |

| [6] | 蔡文武, 陆静, 赵宇洋. 不同市场行情下投资者关注频率对交易驱动的非对称性影响[J]. 中国管理科学, 2023, 31(4): 11-25. |

| [7] | 温锋华, 沈体雁, 邢江波, 寇晨欢. 城市突发公共卫生事件的循证治理机制研究[J]. 中国管理科学, 2023, 31(1): 206-215. |

| [8] | 瞿慧, 沈微. 引入投资者关注的中国股市协方差预测——基于多元HAR类模型[J]. 中国管理科学, 2022, 30(7): 9-19. |

| [9] | 蔡健平, 王晶, 焦子豪. 基于鲁棒优化的突发公共卫生事件精准筛查策略研究[J]. 中国管理科学, 2022, 30(7): 1-8. |

| [10] | 欧阳艳敏, 王长峰, 刘柳, 原宏敏. 基于改进自适应最优分割法的风险预警区间模型研究——针对重大突发公共卫生事件[J]. 中国管理科学, 2022, 30(11): 196-206. |

| [11] | 林娟娟, 唐勇, 周小亮, 朱鹏飞. 北上资金、百度指数与股市关联性的时频域研究——基于协高阶矩视角[J]. 中国管理科学, 2022, 30(1): 20-31. |

| [12] | 瞿慧, 沈微. 基于LSTHAR模型的投资者关注对股市波动影响研究[J]. 中国管理科学, 2020, 28(7): 23-34. |

| [13] | 张同辉, 苑莹, 曾文. 投资者关注能提高市场波动率预测精度吗?——基于中国股票市场高频数据的实证研究[J]. 中国管理科学, 2020, 28(11): 192-205. |

| [14] | 向诚, 陆静. 本地投资者有信息优势吗?基于百度搜索的实证研究[J]. 中国管理科学, 2019, 27(4): 25-36. |

| [15] | 朱学红, 谌金宇, 邵留国. 信息溢出视角下的中国金属期货市场国际定价能力研究[J]. 中国管理科学, 2016, 24(9): 28-35. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||