主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2024, Vol. 32 ›› Issue (6): 34-45.doi: 10.16381/j.cnki.issn1003-207x.2021.2020cstr: 32146.14.j.cnki.issn1003-207x.2021.2020

苏春1( ),刘星2

),刘星2

收稿日期:2021-10-04

修回日期:2022-02-22

出版日期:2024-06-25

发布日期:2024-07-03

通讯作者:

苏春

E-mail:suchongzhi@126.com

基金资助:

Chun Su1(),Xing Liu2

Received:2021-10-04

Revised:2022-02-22

Online:2024-06-25

Published:2024-07-03

Contact:

Chun Su

E-mail:suchongzhi@126.com

摘要:

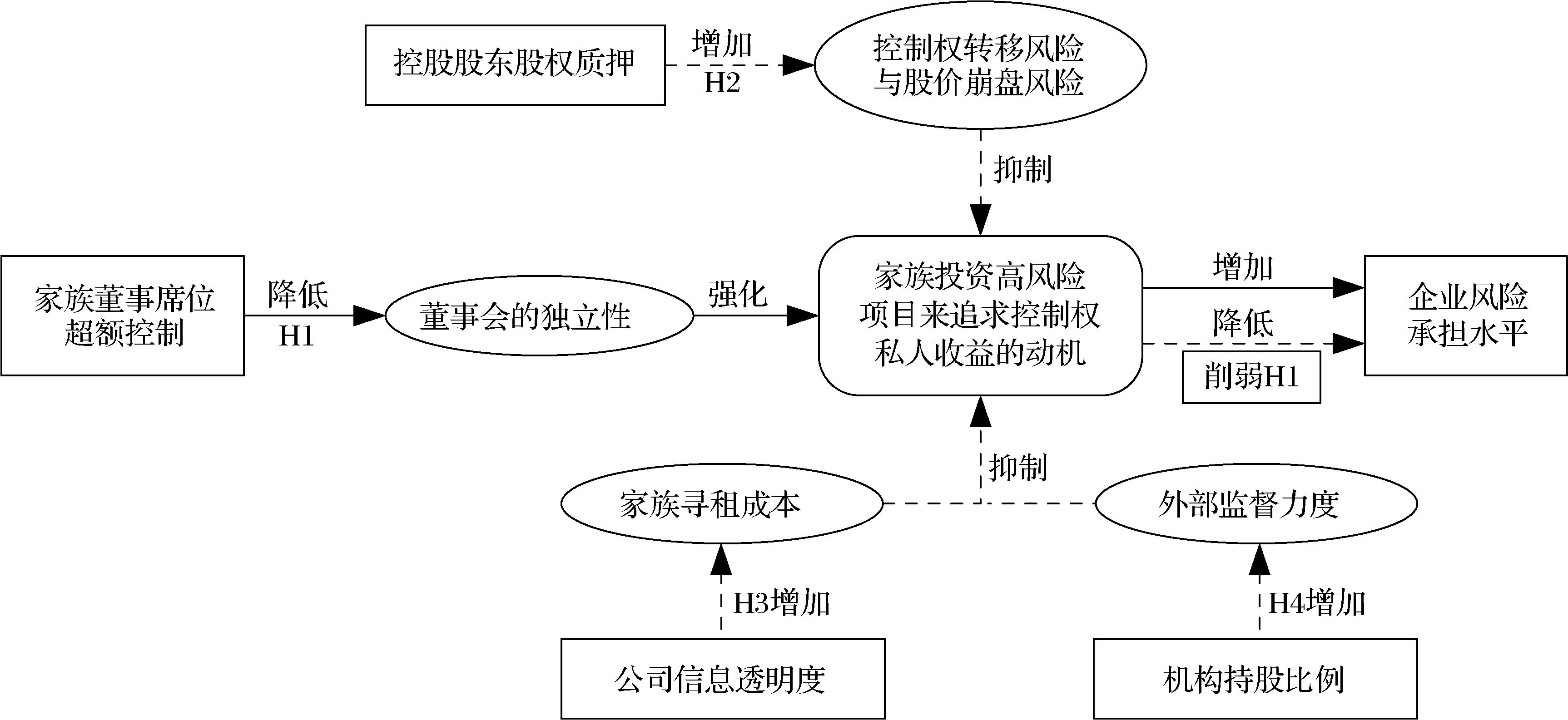

本文以2008-2017年沪深A股上市家族企业为研究样本,考察了家族董事席位超额控制对企业风险承担水平的影响机制及效应。研究发现,家族董事席位超额控制程度与企业风险承担水平显著正相关。进一步分析发现,控股股东股权质押会削弱家族董事席位超额控制程度与企业风险承担水平之间的正相关性;较高的公司信息透明度或者机构持股比例均会降低家族董事席位超额控制程度对企业风险承担水平的正向影响。机制分析表明,控股家族获取控制权私人收益是家族董事席位超额控制影响企业风险承担水平的重要途径。最后,控制潜在的内生性问题,并进行一系列的稳健性检验后,研究结论依然成立。本文不仅丰富和补充了家族董事席位超额控制经济后果的相关研究,也对家族企业的风险投资行为给出了更多的解释。

中图分类号:

苏春,刘星. 家族董事席位超额控制会影响企业风险承担吗?[J]. 中国管理科学, 2024, 32(6): 34-45.

Chun Su,Xing Liu. Does Excess Control of Family Board Seats Affect Corporate Risk-Taking?[J]. Chinese Journal of Management Science, 2024, 32(6): 34-45.

图1

研究假设综合机理"

表1

变量定义"

| 变量名称 | 变量符号 | 变量度量 |

|---|---|---|

| 企业风险承担 | Risk1 | 等于经年度行业均值调整后的Roa的未来三年滚动极差 |

| Risk2 | 等于经年度行业均值调整后的Roa的未来三年滚动标准差 | |

| 家族董事席位超额控制 | ECFBS | 等于家族对公司董事席位控制比例与家族控制权之差 |

| 是否存在股权质押 | Pledge_dum | 家族控股股东年末存在股权质押取值为1,否则取值为0 |

| 股权质押率 | Pledge | 等于家族控股股东质押股票数/家族控股股东持有股票总数 |

| 公司信息透明度 | Transparency | 等于公司年末分析师跟踪人数 |

| 机构持股比例 | InsHold | 等于前十大股东中机构持股比例总和 |

| 公司规模 | Size | 等于Ln(期末总资产) |

| 公司年龄 | Age | 等于Ln(当年年份-公司成立年份) |

| 成长性 | Growth | 等于(本年营业收入-上年营业收入)/上年营业收入 |

| 财务杠杆率 | lev | 等于期末总负债/期末总资产 |

| 两权分离度 | Speration | 等于家族控制权与家族所有权之差 |

| 无形资产占比 | Intangible | 等于期末无形资产/期末总资产 |

| 董事会规模 | Board | 董事会总人数 |

| 独立董事比例 | Indep | 等于独立董事人数/董事会人数 |

| 两职合一 | Dual | 董事长与总经理由一人担任,取值为1,否则取值为0 |

| 家族持股比例 | Fsh | 等于前十大股东中所有家族成员持股比例之和 |

| 地区人均GDP | GDP_per | 等于Ln(各省份人均GDP) |

| 董事长年龄 | Chairman_age | 等于Ln(当年年份-董事长出生年份) |

| 董事长学历 | Chairman_edu | 取值1~5,依次代表中专及以下、大专、本科、硕士、博士学历 |

表2

主要变量的描述性统计"

| 变量 | N | mean | sd | min | p25 | p50 | p75 | max |

|---|---|---|---|---|---|---|---|---|

| Risk1 | 6417 | 0.0603 | 0.0713 | 0.0032 | 0.0205 | 0.0365 | 0.0662 | 0.3778 |

| Risk2 | 6417 | 0.0321 | 0.0388 | 0.0016 | 0.0107 | 0.0191 | 0.0349 | 0.2075 |

| ECFBS | 6417 | -0.0786 | 0.1918 | -0.5587 | -0.2081 | -0.0777 | 0.0549 | 0.3710 |

| Pledge_dum | 6417 | 0.5005 | 0.5000 | 0.0000 | 0.0000 | 1.0000 | 1.0000 | 1.0000 |

| Pledge | 6417 | 0.2970 | 0.3581 | 0.0000 | 0.0000 | 0.0118 | 0.6138 | 1.0000 |

| Transparency | 6417 | 8.2216 | 8.8854 | 0.0000 | 1.0000 | 5.0000 | 12.0000 | 53.0000 |

| InsHold | 6417 | 0.0441 | 0.0445 | 0.0000 | 0.0073 | 0.0308 | 0.0686 | 0.2374 |

表3

主要变量相关性分析"

| 变量 | Risk1 | Risk2 | ECFBS | Pledge_dum | Pledge | Transparency | InsHold |

|---|---|---|---|---|---|---|---|

| Risk1 | 1.0000 | ||||||

| Risk2 | 0.9982*** | 1.0000 | |||||

| ECFBS | 0.0457*** | 0.0458*** | 1.0000 | ||||

| Pledge_dum | -0.1248*** | -0.1267*** | 0.0668*** | 1.0000 | |||

| Pledge | -0.1853*** | -0.1879*** | 0.0930*** | 0.0829*** | 1.0000 | ||

| Transparency | -0.0649*** | -0.0645*** | -0.0452*** | -0.0127 | -0.0767*** | 1.0000 | |

| InsHold | -0.01189*** | -0.0187*** | 0.1149*** | -0.0641*** | -0.0715*** | 0.3642*** | 1.0000 |

表4

家族董事席位超额控制与企业风险承担"

| 变量 | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|---|

| Risk1 | Risk2 | Risk1 | Risk2 | Risk1 | Risk2 | Risk1 | Risk2 | |

| ECFBS | 0.0159** | 0.0087** | 0.0148** | 0.0081** | 0.0200*** | 0.0109*** | 0.0187*** | 0.0102*** |

| (2.10) | (2.12) | (2.02) | (2.04) | (2.73) | (2.76) | (2.61) | (2.63) | |

| Constant | -0.0792 | -0.0479 | -0.0334 | -0.0243 | 0.1080 | 0.0566 | 0.1427* | 0.0741 |

| (-1.07) | (-1.20) | (-0.41) | (-0.55) | (1.39) | (1.33) | (1.72) | (1.63) | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry | NO | NO | Yes | Yes | NO | NO | Yes | Yes |

| Year | NO | NO | NO | NO | Yes | Yes | Yes | Yes |

| N | 6417 | 6417 | 6417 | 6417 | 6417 | 6417 | 6417 | 6417 |

| R2 | 0.0476 | 0.0485 | 0.0649 | 0.0658 | 0.1050 | 0.1057 | 0.1196 | 0.1202 |

表5

家族董事席位超额控制、控股东股权质押与企业风险承担"

| 变量 | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Risk1 | Risk2 | Risk1 | Risk2 | |

| ECFBS | 0.0251*** | 0.0136*** | 0.0214*** | 0.0115*** |

| (3.40) | (3.45) | (2.98) | (3.00) | |

| Pledge_dum | -0.0026*** | -0.0014*** | ||

| (-3.55) | (-3.60) | |||

| Pledge | -0.0042*** | -0.0023*** | ||

| (-4.28) | (-4.36) | |||

ECFBS× Pledge_dum | -0.0075*** | -0.0041*** | ||

| (-2.72) | (-2.72) | |||

ECFBS× Pledge | -0.0055*** | -0.0030*** | ||

| (-2.78) | (-2.75) | |||

| Constant | 0.1378* | 0.0714 | 0.1423* | 0.0738 |

| (1.67) | (1.59) | (1.73) | (1.64) | |

| Controls | Yes | Yes | Yes | Yes |

| Industry& Year | Yes | Yes | Yes | Yes |

| N | 6417 | 6417 | 6417 | 6417 |

| R2 | 0.1187 | 0.1192 | 0.1193 | 0.1198 |

表6

家族董事席位超额控制、公司信息透明度与企业风险承担"

| 变量 | (1) | (2) |

|---|---|---|

| Risk1 | Risk2 | |

| ECFBS | 0.0828*** | 0.0451*** |

| (8.92) | (8.93) | |

| Tansparency | -0.0009*** | -0.0005*** |

| (-3.14) | (-3.13) | |

| ECFBS×Tansparency | -0.0014** | -0.0007** |

| (-2.10) | (-2.06) | |

| Constant | 0.0556 | 0.0256 |

| (0.85) | (0.72) | |

| Controls | Yes | Yes |

| Industry& Year | Yes | Yes |

| N | 6417 | 6417 |

| R2 | 0.1428 | 0.1432 |

表7

家族董事席位超额控制、机构持股比例与企业风险承担"

| 变量 | (1) | (2) |

|---|---|---|

| Risk1 | Risk2 | |

| ECFBS | 0.0756*** | 0.0413*** |

| (7.12) | (7.19) | |

| InsHold | -0.0195 | -0.0108 |

| (-0.79) | (-0.81) | |

| ECFBS×InsHold | -0.0222** | -0.0103* |

| (-2.21) | (-1.92) | |

| Constant | 0.0850 | 0.0419 |

| (1.13) | (1.03) | |

| Controls | Yes | Yes |

| Industry& Year | Yes | Yes |

| N | 6417 | 6417 |

| R2 | 0.1429 | 0.1435 |

表8

影响机制检验"

| 变量 | Tunneling | |||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| ECFBS | 0.0097*** | 0.0088*** | ||

| (3.23) | (3.03) | |||

| Risk1 | 0.0172*** | 0.0268*** | ||

| (3.28) | (3.22) | |||

| Risk2 | 0.0313*** | 0.0524*** | ||

| (3.30) | (3.41) | |||

| ECFBS×Risk1 | 0.0160* | |||

| (1.95) | ||||

| ECFBS×Risk2 | 0.0330** | |||

| (2.18) | ||||

| Constant | 0.0497** | 0.0473** | 0.0440** | 0.0499** |

| (2.09) | (2.16) | (1.98) | (2.28) | |

| Controls | Yes | Yes | Yes | Yes |

| Industry& Year | Yes | Yes | Yes | Yes |

| N | 6417 | 6417 | 6417 | 6417 |

| R2 | 0.0254 | 0.0325 | 0.0253 | 0.0357 |

表9

工具变量有效应检验及回归结果"

| 变量 | (1) | (2) | (3) | (4)sargen test | (5)sargen test | (6)2SLS | (7)2SLS |

|---|---|---|---|---|---|---|---|

| Risk1 | Risk2 | ECFBS | Risk1 | Risk2 | |||

| ECFBS_indaverage | 0.0736 | 0.0379 | 0.5421*** | 0.0604 | 0.0308 | ||

| (1.27) | (1.19) | (7.33) | (1.43) | (1.35) | |||

| ECFBS_proaverage | 0.0140 | 0.0092 | 0.1467*** | -0.0154 | -0.0072 | ||

| (0.55) | (0.67) | (5.83) | (-0.81) | (-0.71) | |||

| ECFBS | 0.0192*** | 0.0104*** | 0.1093** | 0.0599** | |||

| (2.68) | (2.70) | (2.26) | (2.32) | ||||

| Constant | 0.1394* | 0.0721 | 0.0115*** | 0.0322 | 0.0172 | 0.2701*** | 0.1446*** |

| (1.67) | (1.58) | (6.52) | (0.68) | (0.67) | (5.49) | (5.44) | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry& Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 6417 | 6417 | 6417 | 6417 | 6417 | 6417 | 6417 |

| R2 | 0.1205 | 0.1211 | 0.4846 | 0.0019 | 0.0018 | 0.1163 | 0.1150 |

表10

基于增加控制变量的内生性检验"

| 变量 | (1) | (2) |

|---|---|---|

| Risk1 | Risk2 | |

| ECFBS | 0.0136** | 0.0074** |

| (2.03) | (2.05) | |

| Constant | 0.1445* | 0.0737* |

| (1.85) | (1.75) | |

| Controls | Yes | Yes |

| Industry&Year | Yes | Yes |

| N | 6417 | 6417 |

| R2 | 0.1217 | 0.1228 |

| 1 | Lumpkin G T, Dess G G.Clarifying the entrepreneurial orientation construct and linking it to performance[J].The Academy of Management Review,1996,21(1):135-172. |

| 2 | 余明桂,李文贵,潘红波.管理者过度自信与企业风险承担[J].金融研究,2013(1):149-163. |

| Yu M G, Li W G, Pan H B. Managerial overconfidence and enterprise risk-taking[J]. Journal of Financial Research,2013(1):149-163. | |

| 3 | Morck R, Shleifer A, Vishny R W. Management ownership and market valuation:An empirical analysis[J].Journal of Financial Economics,1988,20(88):293-315. |

| 4 | Beasley M S.An empirical analysis of the relation between board of director composition and financial Statementfraud[J].The Accounting Review,1996,71(4):443-465. |

| 5 | Akbar S, Kharabsheh B, Poletti-Hughe J,et al. Board structure and corporate risk taking in the UK financial sector[J].International Review of Financial Analysis,2017,50(C):101-110. |

| 6 | 孟焰,赖建阳.董事来源异质性对风险承担的影响研究[J].会计研究,2019(7): 35-42. |

| Meng Y, Lai J Y. The influence of directors’ sources diversity on risk-taking[J].Accounting Research,2019(7):35-42. | |

| 7 | Villalonga B, Amit R.How are U.S. family firms controled?[J].Review of Financial Studies,2009,22(8):3047-3091. |

| 8 | Amit R, Ding Y, Villalonga B,et al. The role of instituteonal development in the prevalence and performanceof entrepreneur and family-controlled firms[J]. Journal of Corporate Finance,2015,31:284-305. |

| 9 | 刘星,苏春,邵欢. 家族董事席位配置偏好影响企业投资效率吗[J].南开管理评论,2020,23(4):131-141. |

| Liu X, Su C, Shao H. Does the preference of family board seats allocation influence corporate investment efficiency[J]. Nankai Business Review,2020,23(4):131-141. | |

| 10 | 刘星,苏春,邵欢. 家族董事席位超额控制与股价崩盘风险——基于关联交易的视角[J].中国管理科学,2021,29(5):1-13. |

| Liu X, Su C, Shao H. Excess control of family board seats and stock price crash risk:Based on the perspective of related party trasactions[J]. Chinese Journal of Management Science,2021,29(5):1-13. | |

| 11 | 陈德球,魏刚,肖泽忠.法律制度效率、金融深化与家族控制权偏好[J].经济研究,2013,48(10):55-68. |

| Chen D Q, Wei G, Xiao Z Z. Law efficiency,financial deepening and family control preferences[J]. Economic Research Journal,2013,48(10):55-68. | |

| 12 | 刘星,苏春,邵欢. 代际传承与家族董事席位超额控制[J].经济研究,2021,56(12):111-129. |

| Liu X, Su C, Shao H. Intergenerational successsion and excess control of family board seats[J]. Economic Research Journal,2021,56(12):111-129. | |

| 13 | 陈德球, 叶陈刚, 李楠.控制权配置、代理冲突与审计供求——来自中国家族上市公司的经验证据[J].审计研究, 2011(5):57-64. |

| Chen D Q, Ye C G, Li N. Control rights allocateion,agency conflicts and auditor demand and supply:Empirical evidence from the Chinese family listed companies[J]. Auditing Research,2011(5):57-64. | |

| 14 | 陈德球,李思飞,雷光勇.政府治理、控制权结构与投资决策——基于家族上市公司的经验证据[J].金融研究,2012(3)124-138. |

| Chen D Q, Li S F, Lei G Y. Governance,controlstructure and investment decision: Empirical evidence from family listed firm[J]. Journal of Financial Research,2012(3):124-138. | |

| 15 | 陈德球,肖泽忠,董志勇.家族控制权结构与银行信贷合约:寻租还是效率?[J].管理世界,2013(9):130-143. |

| Chen D Q, Xao Z Z, Dong Z Y. The composition of the family control rights and the credit contract of banks: Is it rent-seeking or efficiency?[J]. Management World,2013(9):130-143. | |

| 16 | 赵宜一,吕长江.家族成员在董事会中的角色研究——基于家族非执行董事的视角[J].管理世界,2017(9):155-165. |

| Zhao Y Y, Lv C J. Research on the role of family members in the board from the perspective of the family’s non: Executive directors[J].Management World,2017(9):155-165. | |

| 17 | 于洪涛.董事会特征、风险承担与公司绩效[D].大连:东北财经大学,2019. |

| Yu H T. Board characteristics,risk-taking and corporation performance[D]. Dalian:Dongbei University of Finance and Economics,2019. | |

| 18 | Wang C J.Board size and firm risk-taking[J].Review of Quantitative Finance and Accounting,2012,38(4):519-542. |

| 19 | Cheng S.Board size and the variability of corporate performance[J].Journal of Financial Economics,2008,87(1):157-176. |

| 20 | Nakano M, Nguyen P.Board size and corporate risk taking:Further evidence from Japan[J]. Corporate Governance:An International Review,2012,20(4):369-387. |

| 21 | Bernile G, Bhagwat V, Yonker S.Board diversity,firm risk,and corporate policies[J]. Journalof Financial Economics,2018,127(3):588-612. |

| 22 | 姜付秀,郑晓佳, 蔡文婧.控股家族的“垂帘听政”与公司财务决策[J].管理世界, 2017(3):125-145. |

| Jiang F X, Zheng X J, Cai W J. Controlling family’s“from behind the curtain”and company’s financial decision[J]. Management World,2017(3):125-145. | |

| 23 | Chua J H, Chrisman J J, Sharma P.Defining the family business by behavior[J].Entrepreneurship Theory and Practice,1999,23(4):19-39. |

| 24 | Jensen M C, Meckling W H.Theory of the firm:Managerial behavior,agency costs and ownership structure[J].Journal of Financial Economics,1976,3(4):305-360. |

| 25 | Ali A, Chen T, Radhakrishnan S. Corporate disclosures by family firms[J]. Journal of Accounting and Economics,2007,44(1-2): 238-286. |

| 26 | La Porta R, Lopez-De-Silanes F, Shleifer A. Corporate ownership around the world[J]. Journal of Finance,1999,54(2):471-517. |

| 27 | 马磊,徐向艺.两权分离度与公司治理绩效实证研究[J]. 中国工业经济,2010(12):108—116. |

| Ma L, Xu X Y. Empirical study on the relationship between the separation degree and corporate governance performance[J].China Industrial Economics,2010(12):108-116. | |

| 28 | Johnson S, La Porta R, Lo’Pez-De-Silanes F,et al. Tunneling[J]. American Economic Review,2000,90(2):22-27. |

| 29 | 李常青,李宇坤,李茂良.控股股东股权质押与企业创新投入[J].金融研究,2018(7):143-157. |

| Li C Q, Li Y K, Li M L. Control shareholder’s share pledge and firms’ innovation investment[J]. Journal of Financial Research,2018(7):143-157. | |

| 30 | 谢德仁,郑登津,崔宸瑜.控股股东股权质押是潜在的“地雷”吗?——基于股价崩盘风险视角的研究[J].管理世界, 2016(5):128-140. |

| Xie D R, Zheng D J, Cui C Y. Is controlling Shareholder’s share pledge a potential“mine”: Research based on the perspective of stock price crash risk[J]. Management World,2016(5):128-140. | |

| 31 | 何威风,刘怡君,吴玉宇.大股东股权质押和企业风险承担研究[J].中国软科学, 2018(5):110-122. |

| He W F, Liu Y J, Wu Y Y. Research on the pledging of stock rights by large shareholders and corporate risk-taking[J]. China Soft Science,2018(5):110-122. | |

| 32 | 王克敏,姬美光,李薇.公司信息透明度与大股东资金占用研究[J].南开管理评论, 2009,12(4):83-91. |

| Wang K M, Ji M G, Li W. Corporate transparency and expropriation by large shareholders[J]. Nankai Business Review,2009,12(4):83-91. | |

| 33 | Lin C, Ma Y, Malatesta P,et al. Corporate ownership structure and bank loan syndicate structure[J]. Journal of Financial Economics,2012,104(1):1-22. |

| 34 | Chaganti R, Damanpour F.Institutional ownership,capital structure,and firm performance[J]. Strategic Management Journal,1991,12(7):479-491. |

| 35 | Ajinkya B, Bhojraj S, Sengupta P.The association between outside directors,institutional investors and the properties of management earnings forecasts[J].Journal of Accounting Research,2005,43(3):343-376. |

| 36 | 石美娟,童卫华.机构投资者提升公司价值吗?——来自后股改时期的经验证据[J].金融研究,2009(10):150-161. |

| Shi M J, Tong W H. Do institutional investors increase company value:Empirical evidence from the postshare Reform Period[J]. Journal of Financial Research,2009(10):150-161. | |

| 37 | Xu N, Yuan Q, Jiang X,et al.Founder`s political conections,second generation involvement,and family firm performance:Evidence from China[J]. Journal of Corporate Finance,2015,33(3):243-259. |

| 38 | 刘白璐,吕长江.中国家族企业家族所有权配置效应研究[J].经济研究,2016,51(11):140-152. |

| Liu B L, Lv C J. The effect of ownership structure among family members in Chinese family fiirms[J].Economic Research Journal,2016,51(11): 140-152. | |

| 39 | Anderson R C, Reeb D M. Founding-family ownership and firm performance:Evidence from the S&P 500[J].The Journal of Finance,2003,58(3):1301-1327. |

| 40 | 巩键,陈凌,王健茜,等.从众还是独具一格?——中国家族企业战略趋同的实证研究[J].管理世界,2016(11):110-124. |

| Gong J, Chen L, Wang J X,et al. Follow the crowd or keep unique:An empirical study on the strategic convergence of Chinese family firms[J]. Management World,2016(11):110-124. | |

| 41 | Coles J L, Daniel N D, Naveen L. Managerial incentives and risk-taking[J]. Journal of Financial Economics,2006,79(2):431-468. |

| 42 | 王元芳,徐业坤.保守还是激进:管理者从军经历对公司风险承担的影响[J].外国经济与管理,2019,41(9):17-30. |

| Wang Y F, Xu Y K. Conservative or radical: The influence of managers’ military experience on the company’s risk-taking[J]. Foreign Economics & Management,2019,41(9):17-30. | |

| 43 | John K, Litov L, Yeung B.Corporate governance and risk-taking[J]. Journal of Finance,2008,63(4):1679-1728. |

| 44 | Faccio M, Marchica M T, Mura R. Large shareholder diversification and corporate risk-taking[J]. Review of Financial Studies,2011,24(11):3601-3641. |

| 45 | 肖金利,潘越,戴亦一.“保守”的婚姻:夫妻共同持股与公司风险承担[J].经济研究,2018,53(5):190-204. |

| Xiao J L, Pan Y, Dai Y Y. Marriage of “conservative”:Couples’ joint holdings and corporate risk-taking[J]. Economic Research Journal,2018,53(5):190-204. | |

| 46 | Bharath S T, Dahiya S, Saunders A,et al.Lendingrelationships and loan contract terms[J].Review of Financial Studies,2011,24(4):1141-1203. |

| 47 | 陈爽英,井润田,龙小宁,等.民营企业家社会关系资本对研发投资决策影响的实证研究[J].管理世界,2010(1):88-97. |

| Chen S Y, Jing R T, Long X N,et al. An empirical study on the impact of private entrepreneurs’ social relationship capital on R&D investment decisi-ons[J]. Management World,2010(1):88-97. |

| [1] | 陈小辉, 张红伟, 文佳, 吴永超. FinTech信贷规模能刺激金融机构提升涉农贷款占比吗?[J]. 中国管理科学, 2022, 30(5): 76-85. |

| [2] | 于辉, 王琪. 风险承担机制视角下企业汇率管理的供应链分析[J]. 中国管理科学, 2021, 29(9): 44-53. |

| [3] | 刘星, 苏春, 邵欢. 家族董事席位超额控制与股价崩盘风险——基于关联交易的视角[J]. 中国管理科学, 2021, 29(5): 1-13. |

| [4] | 田银华, 周志强, 廖和平, 李石新. 基于BP神经网络的家族企业契约治理模式识别与选择研究[J]. 中国管理科学, 2011, 19(1): 159-166. |

| [5] | 王明好, 陈忠, 蔡晓钰. 相对业绩对投资基金风险承担行为的影响研究[J]. 中国管理科学, 2004, (5): 1-5. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||